On June 10, the CFTC sketched a formal 90‑day review track for controversial event contracts. Within weeks, Polymarket’s U.S. affiliate quietly filed for parlay‑style sports markets, and Kalshi secured a first‑of‑its‑kind perpetual futures approval.

For the first time, there’s a visible lane where sports prediction markets could graduate from grey‑area experimentation to regulated scale—if they can clear new tests on lawfulness, integrity, and public interest.

Winners won’t be decided by hype, but by who can operate like a derivatives exchange and a gaming venue at the same time.

Editor’s note: The Appendix F conversations are pragmatic: exchanges are building surveillance around league‑grade data and rethinking position limits for outcomes that can swing on a tweet. The Kalshi BTCPERP approval confirmed that creative structures win if the plumbing is solid, but sports adds a public‑interest layer that’s not negotiable. The Polymarket US combinatorial angle is clever for liquidity, yet it multiplies risk if the margin math or data rights are shaky. If sports goes live, it will be with training wheels and lots of stopgaps. — Maya Sinclair

The CFTC’s Notice of Proposed Rulemaking (Release No. 9249‑26) would amend Regulation 40.11 and add an Appendix F that outlines a contract‑by‑contract 90‑day review for event contracts that may involve areas like terrorism, war, assassination, and gaming—topics historically shut down or forced into ad‑hoc determinations. The move arrives as U.S. venues circle sports outcomes under the “event contract” umbrella.

The proposal doesn’t legalize sports betting; it defines a decision process for which event contracts a CFTC‑regulated exchange may list, and under what conditions, without violating federal or state law.

Two developments underscore the timing: QCX LLC (Polymarket US) submitted a confidential product self‑certification for “Combinatorial Athletic Outcome Contracts” on May 20, 2026 (CFTC FOIA filing), and nine days later, on May 29, 2026, the CFTC approved KalshiEX LLC’s BTCPERP perpetual futures contract—the first perpetual product greenlit on a U.S. CFTC‑regulated venue (CFTC order). Meanwhile, on May 27, 2026, the agency filed an insider‑trading complaint tied to trades on Polymarket, signaling the enforcement backdrop that will shape any expansion (CFTC press release).

How Regulation 40.11 Has Contained Event Markets

Regulation 40.11 has long been the brake pedal on event contracts that “involve” unlawful activity under federal or state law, or that threaten the public interest. Exchanges typically steer clear of elections, assassination, or gaming narratives unless they can make a rock‑solid case that the contract is lawful and socially acceptable.

Why sports get sucked into the “gaming” filter

Sports outcomes resemble wagers more than hedges. Even when contracts are sized like derivatives and margined like futures, regulators have to be comfortable that a listing does not contravene state gambling prohibitions or the Wire Act, and that it serves a legitimate risk‑management purpose. The proposed Appendix F wouldn’t flip a switch; it would sequence a transparent, case‑by‑case review.

What the June 10 proposal would change

Per the CFTC’s June 10, 2026 release, the agency aims to build a structured 90‑day determination process with specific factors and public‑interest analysis for sensitive categories, including gaming (CFTC press release). That’s a potential gateway for sports contracts to be evaluated on their own merits instead of by blanket skepticism.

Polymarket US’s Parlay Bid: What “Combinatorial” Really Means

QCX LLC, the U.S. entity associated with Polymarket, filed a product self‑certification on May 20 for “Combinatorial Athletic Outcome Contracts” (CAOCs), seeking confidential treatment. The label suggests parlay‑style structures that pay based on multiple legs—e.g., Team A wins and Player X scores over N points—collapsed into a single payoff schedule. That’s a leap in market design, not just another moneyline.

What the filing does—and doesn’t—imply

The FOIA record shows a submission and confidentiality request, not an approval or launch. The substance of CAOCs, including how they clear the lawfulness test and surveillance standards, still has to pass muster (CFTC FOIA filing).

Why combinatorics matter for liquidity

Combinatorial markets let venues concentrate liquidity in popular multi‑leg views while pricing correlated outcomes more efficiently than separate silos. If allowed, they could compress spreads and improve discovery for complex fan and trader beliefs—core to scaling beyond simple yes/no markets.

- Venue drafts contract specs, surveillance, and risk controls for a combinatorial book.

- Submission hits the CFTC portal, with or without a confidential attachment.

- Under the proposal, contracts that may involve gaming trigger a 90‑day review with public‑interest analysis.

- The Commission evaluates lawfulness, manipulation risk, and hedging rationale under Appendix F.

- If cleared, the contract self‑certifies or is approved for listing; if not, it’s stayed or withdrawn.

Kalshi’s Perpetual Milestone Is A Signal—Not A Shortcut—for Sports

Kalshi’s BTCPERP approval on May 29 put a U.S. CFTC‑regulated exchange in the business of listing a perpetual futures product for the first time. This indicates the Commission will bless novel structures if the risk, custody, and market‑integrity plumbing are tight (CFTC order).

Signal vs. substance

Perpetuals are still financial futures; sports are “event contracts” with a gaming overlay. BTCPERP doesn’t pave a legal lane for sports by itself, but it proves a sponsor can win approval for an innovative format by handling margin, index methodology, conflicts, and surveillance. The bar for sports will include those plus fit‑with‑law questions.

Enforcement Is The Gravity: A Polymarket Insider‑Trading Case

On May 27, 2026, the CFTC alleged a Google software engineer traded on nonpublic information tied to “Year in Search” outcomes on Polymarket, earning approximately $1.2 million; SDNY unsealed a parallel criminal complaint the same day (CFTC press release). The facts will be litigated, but the message is simple: event contracts attract material nonpublic information (MNPI), just like equities and commodities—and regulators will treat them accordingly.

What this means for regulated sports markets

Any exchange seeking sports listings will need surveillance that understands player injuries, lineup changes, and leaked data feeds; position limits and fast halts around breaking news; and cooperative agreements with leagues and data providers. The enforcement drumbeat makes Appendix F’s “public interest” lens more stringent, not less.

Who Stands Where: Designs, Licenses, and Likely Paths

Sports prediction at regulated scale will reward venues that look like true exchanges, not casual apps. That means: robust KYC/AML, enumerated position limits, clearing arrangements, transparent rulebooks, market‑maker programs, and surveillance baked into contract design.

At‑a‑glance comparison

| Dimension | KalshiEX (DCM) | QCX LLC (Polymarket US) | Polymarket.com (global) |

|---|---|---|---|

| Regulatory posture | CFTC‑regulated Designated Contract Market | U.S. affiliate; filed product self‑cert for CAOCs; approval pending | Offshore prediction market; access varies by jurisdiction |

| Recent milestone | BTCPERP perpetual approved May 29, 2026 | CAOC filing dated May 20, 2026 (confidential request) | Faced CFTC scrutiny in the past; continues operating globally |

| Primary product style | Event contracts; now perpetuals referencing bitcoin | Proposed combinatorial (parlay‑style) sports contracts | Binary markets across sports, politics, culture |

| Biggest gating factor for sports | Appendix F review on gaming; state/federal law fit | Same, plus demonstrating surveillance for combinatorics | U.S. access constraints; regulatory risk |

How this could play out

If the CFTC finalizes the 90‑day review with clear criteria, DCMs and would‑be DCMs will likely sequence a handful of low‑controversy sports markets—win/loss, season totals tied to public stats—before experimenting with complex parlays. Expect partnerships with data providers to shore up settlement integrity and anti‑manipulation screens.

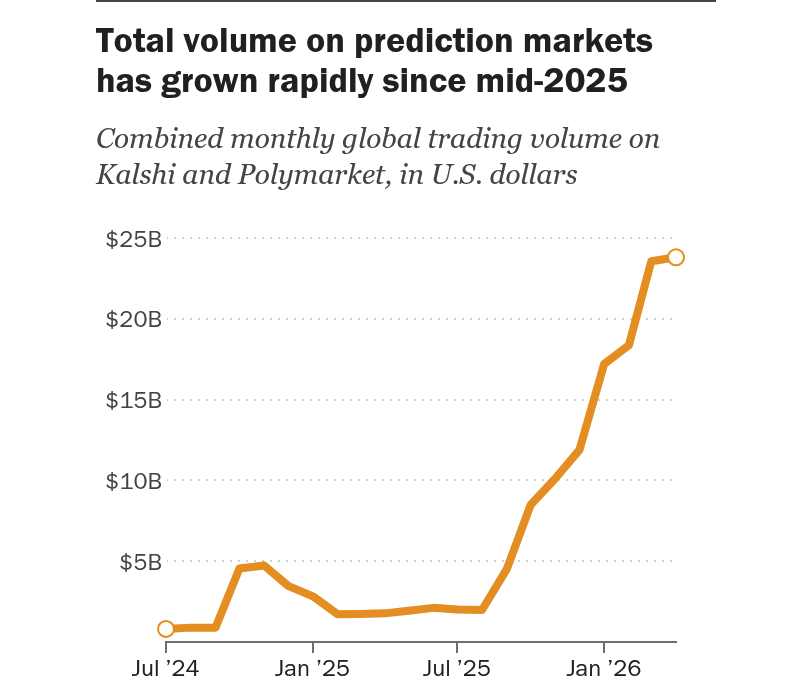

Combined monthly global trading volume on Kalshi and Polymarket (Jul 2024–Apr 2026); shows a sharp rise into 2026 and illustrates the scale driving recent CFTC rulemaking and product filings. — Source: Pew Research Center (chart, May 27, 2026)

What A Regulated Sports Market Might Actually Look Like

Assuming Appendix F becomes operational, here’s what a compliant product likely entails.

Contract design and settlement

- Outcomes tied to league‑verified data (e.g., official box scores) with pre‑announced ties and cancellation rules.

- Position limits that scale down near game time; automatic pauses on data feed anomalies.

- Clear definitions for suspended or postponed games to prevent “information arbitrage.”

Market integrity stack

- KYC/AML across all participants; heightened review for affiliates of teams, leagues, or data vendors.

- Surveillance tuned to sports‑specific signals: injury reports, credentialed media leaks, and data latency patterns.

- Information‑barrier policies and reporting obligations for traders with potential MNPI.

Risk and margin

- Real‑time margin for combinatorial exposures, with laddered haircuts for correlated legs.

- Market‑maker programs that quote both legs and combined outcomes to keep spreads tight.

- Kill‑switches for orphaned combinations if a leg becomes unlistable (e.g., canceled game).

Risks & What Could Go Wrong

- Regulatory reversal: The final rule could narrow Appendix F, barring most sports contracts or imposing conditions that make them uneconomic.

- State law preemption: Even if federally permitted, conflicting state gambling rules could limit distribution or force geofencing, shrinking liquidity.

- Data dependency: Settlement tied to proprietary feeds creates single‑point failures or rent‑seeking through costly licenses.

- MNPI leakage: Team insiders, data vendors, or platform employees may exploit nonpublic info without robust barriers and audits.

- Public backlash: High‑profile manipulation or scandal could sour policymakers and tighten restrictions.

- Operational complexity: Combinatorial books can magnify exposure and margin errors if risk systems aren’t battle‑tested.

If sports contracts launch before surveillance, data rights, and position‑limit frameworks are mature, the first blow‑up will set the rules for years.

For ongoing, source‑driven coverage of rulemakings, filings, and enforcement shaping prediction markets, Crypto Daily tracks primary documents and industry responses in real time at cryptodaily.co.uk.

Frequently Asked Questions

Does the CFTC proposal legalize sports betting in the U.S.?

No. It creates a review process for whether specific event contracts can be listed by CFTC‑regulated exchanges without violating federal or state law. Sports contracts would still need to pass a lawfulness and public‑interest test.

What exactly did Polymarket US file?

QCX LLC submitted a product self‑certification labeled “Combinatorial Athletic Outcome Contracts” and requested confidentiality for the details. It is not an approval or launch; it signals intent and starts a regulatory process.

Why is Kalshi’s BTCPERP approval relevant to sports?

It shows the CFTC will approve innovative formats when risk controls and market integrity are strong. But sports face additional hurdles under Regulation 40.11 and the proposed Appendix F.

How would the 90‑day review work?

Under the June 10, 2026 proposal, contracts involving sensitive categories like gaming could be examined for up to 90 days, weighing lawfulness, manipulation risk, and public interest before listing decisions.

Could insider trading rules apply to sports prediction markets?

Yes. The CFTC’s May 27, 2026 complaint tied to Polymarket highlights that trading on material nonpublic information—like confidential data about outcomes—can trigger civil and criminal actions.

Will parlay‑style contracts be allowed?

They could be, if they satisfy the CFTC’s lawfulness, integrity, and risk‑management standards and do not conflict with state or federal law. Approval is not guaranteed.

When might we see the first regulated sports contracts?

Timing depends on the finalization of the rule, the specifics of submitted products, and any state‑law frictions. A cautious, limited rollout is more likely than a broad launch.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Credit: Source link